Market Overview – Week 18/24

2024-05-03

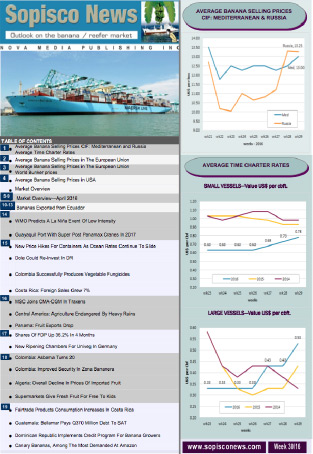

Banana selling prices in St. Petersburg fluctuated significantly throughout the week, influenced by factors such as brand, volume, quality, and packaging. Prices began at USD 22.50 per box CIF on Monday, increased to USD 23.55 on Tuesday, and escalated to USD 24.65 per box CIF by Thursday. One container vessel with around 485.000 boxes will be delayed to the incoming week. Despite these price fluctuations, demand remained consistent during the extended holiday period.

In week 18, approximately 1.52 million boxes were unloaded, and an estimated 2.15 million boxes are projected for week 19. This increasing demand trend is a positive indicator for the industry, although demand is anticipated to decline in the upcoming weeks, as is typical when summer fruits enter the market.

Interestingly, a substantial volume of bananas from China made their way into the Central Asian former Soviet Republics. While bananas from other sources are also regularly imported into Russia, the preference continues to favor Ecuadorian fruit, indicating a promising market for Ecuadorian banana exporters.

The exchange rate was established at 1 USD = 91.79 RUB.

In the Mediterranean, Ecuadorean bananas were priced between USD 16.0 and USD 18.0 per box CIF. Brand, quality, packing, and volume influenced these prices. In contrast, Central American bananas were sold for approximately USD 2.0 less per box. In Libya, Ecuadorean bananas were priced at USD 19.0 per box CIF, while Central American bananas were priced at USD 17.0 per box.

In the Mersin Free Zone, re-exported Ecuadorean bananas were priced between USD 17.0 and USD 18.0 per box. However, sales were also made at lower and higher prices for fruit of extra quality and higher weight. Central American bananas were priced between USD 13.50 and USD 15.0 per box.

As reported by local traders, sales volumes were lower than the previous week, and selling became more challenging due to some unsold quantities. Traders are preparing for the anticipated lower volumes in the coming weeks due to weaker demand in neighbouring countries and the domestic markets of Turkey and Iran. This is attributed to the anticipated influx of large volumes of local summer fruit, which will be more competitively priced than imported fruit. The constant devaluation of regional currencies against the USD further exacerbates the situation, making imported fruit increasingly expensive.

The exchange rate was 1 USD=32.33 TL.

The Iranian domestic market prices also fell due to the influx of large quantities of low-quality bananas from India. The import of bananas from Pakistan is expected to soon increase, which will further negatively impact prices.

The prevailing prices for bananas during the week were around 60.000-66.000 Toman per kg for Ecuadorean bananas and around 45.000-55.000 Toman per kg for Indian bananas.

The cost of a 13.50 kg box of Indian bananas, FOB Nhava Sheva, was approximately USD 5.50. The freight rate, which plays a significant role in the final price, was around 4,400 per reefer FEU to Bandar Abbas. Local traders anticipate a decrease in shipments from India in the upcoming weeks, which could potentially impact the market.

The exchange rate was 1 USD = 62.000 Toman.

The Ecuadorian Spot Market prices rose swiftly from USD 8.0-8.50 per box for the fruit only at the start of the week to USD 9.50-10.0 per box in the following days. This price variation depended on factors like quality, volume, and the region of fruit origin. The abbreviated week impacted the operations, as Friday was declared a holiday instead of Wednesday to observe the 1st of May festivities.

In the Chartering Market, a vessel with a capacity of about 145,000 boxes, which had been idle in Ecuador for a long time, was fixed to undertake a voyage from Guayaquil to Poland. There was uncertainty throughout the week regarding whether the vessel would be loaded in Guayaquil, Puerto Bolivar, or both ports.

The vessel might have been chartered due to the significant loss of banana volumes in Turbo caused by strong winds and floods, or simply to take advantage of better freight rates compared to containers.

Several vessels were engaged in the citrus trade in South Africa for Russia, Northern Europe, and the USA. The squid season in the Southern Atlantic and the Falklands concluded, while numerous vessels are involved in the New Zealand kiwi trade to various global destinations. The fish trade from the Faroes and Northern Europe to West Africa also employed several ships.

The Time Charter rates were US Cents 80-85 per cbft per month for larger ships and approximately US Cents 75-80 for smaller ships.

Bunker Prices:

VLSFO MGO

Rotterdam $574.00 $738.50

Gibraltar $612.00 $803.00

Panama - $787.00