Market Overview – Week 05 / 2024

2024-02-02

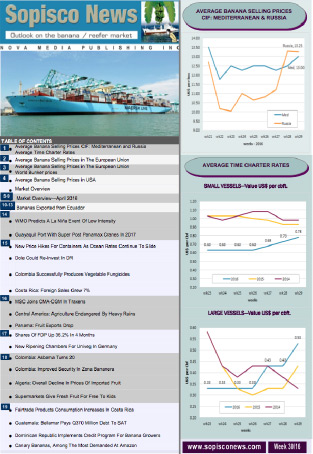

Banana selling prices in St Petersburg dropped compared to the past week, and according to brand, volume and packing, the main prices were USD 17.25-21.70 per box CIF.

Nearly 1.5 million boxes were discharged in week five, and around 1.56 million are expected for week 6.

The exchange rate was 1 USD=90.66 RUB.

The Mediterranean prices for Ecuadorian bananas were USD 15.00-16.00 per box CIF according to brand, volume, and region.

Prices in Libya for Ecuadorian bananas were around USD 17.0 per box CIF and USD 15.0-16.0 per box CIF for Central American bananas.

Prices in Algeria were also around USD 17.0 per box CIF. Some importers incurred losses from the bananas in the previous weeks when the prices were much higher than now at the origin.

The Mersin Free Zone prices for the re-exported bananas of Ecuadorian origin were USD 15.0-17.0 according to brand, quality, packing and weight and around USD 13.0-14.0 per box for Central American bananas.

The exchange rate was 1 USD=30.34 TL.

In the Iranian domestic market, the price for yellow bananas from Ecuador was around 65.000 -70.000 Toman per kg for

Indian bananas, around 45.000- 50.000 Toman per kg, and 40.000-55.000 Toman per kg for the Philippines origin.

The 13.50 kg box of Indian bananas was USD 9.0-9.25 per box CIF Bandar Abbas. The exchange rate was 1 USD=59.000 Toman, a devaluation of almost 20%, which affected sales.

A further devaluation of the Iranian currency caused mainly by the geopolitical events in the Red Sea could severely affect the bananas imports of the Islamic Republic.

Ecuadorian Spot Market prices were USD 7.00-7.50 per box for the fruit only, mainly during the week.

Prices were lower than the previous week as some vessels of the weekly liner service were delayed, and larger volumes of bananas were available.

However, the main reason for the drop in prices was the considerable increase in fruit production due to higher temperatures and regular rains in all producing areas.

According to industry sources, the bagging is very high, and it increased a lot in week five and is expected to remain at high levels for the long term. Stems per bag in some areas were 45-50 recently, while the previous year, at the same time, were 30-35.

One additional reason for the high volumes of fruit available in the Spot market is that warlike activities in the Red Sea, which caused longer trips from Ecuador to destinations in the Middle East, Jebel Ali in the UAE, Umm Qasr in Iraq and elsewhere there and the higher freight rates of around USD 1,500-2.000 per container for exports to those destinations stopped. One of the largest traders to those regions alone has dropped shipments from around 300 containers to 100.

Some sources mention that volumes which used to go to the ME were up to 500.000 boxes per week. Shipments to Jeddah have not been affected as apparently there is a feeder service from the Mediterranean, and the Northern part of the Red Sea is not affected by the Houthis drones and missile attacks.

There were rumours that one of the traders for the Mediterranean might load a Specialised Reefer Vessel to Algeria, although it remains to be confirmed.

No banana fixtures were put on record; however, one vessel might have been fixed for a shipment from Ecuador to Algeria, which remains to be confirmed.

One Seatrade ship, the Cold Stream, with citrus cargo from Turkey to Japan via the Suez Canal, reportedly managed to transit the Red Sea safely and is currently underway to its final destination.

Time Charter for larger vessels stood at US Cents 75-80 per cbft per month and around US Cents 65-75 per cbft per month, although small-size vessels still reported idle awaiting order.

Bunker Prices:

VLSFO MGO

Gibraltar $635.00 $975.00

Rotterdam $584.00 $816.00

Panama Canal $609.00 $1065.00