Market Overview – Week 03/25

2025-01-17

In week 03, approximately 2.17 million boxes of bananas were discharged in St. Petersburg, which was considered a significant volume given the weak demand following the long holiday period. The primary prices ranged from USD 16.70 to 17.65 per box CIF depending on the brand, volume, and packaging.

The expected volume for week 04 is 1.35 million boxes. As for the exchange rate, it stood at 102.38 RUB to the US Dollar.

The Russian Ruble has experienced notable fluctuations over the past weeks. As of January 17, 2025, the Ruble traded at approximately 102.47 to the US Dollar, marking a slight improvement from its lowest point of 115 to the US Dollar on January 1, 2025. However, it has recently been weakening again. Various factors, including sanctions, inflationary pressures, and economic policies, have affected the value of the Ruble.

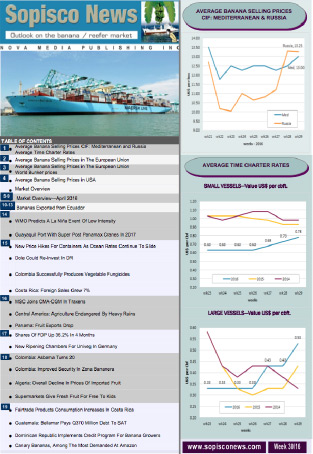

Selling prices for Ecuadorean bananas in the Mediterranean ranged from USD 14.00 to USD 15.00 per-box, cost, insurance, and freight (CIF). In Libya, however, prices were higher at USD 16.00 per-box CIF for Ecuadorean bananas. For Central American bananas, the prices were approximately USD 14.00 per box CIF.

In Algeria, prices were slightly lower compared to previous weeks, with sales of 19.50 kg boxes of Ecuadorean bananas priced around USD 22.00 to USD 23.00 per box CIF.

In the Mersin Free Zone, prices for re-exported bananas of Ecuadorean origin to neighbouring countries ranged from USD 14.50 to USD 16.00 per box, depending on the brand, volume, weight, and packaging. Central American bananas were sold at about USD 2.00 less per carton.

The Iranian domestic market largely followed the trend from the previous week. Prices initially improved at the beginning of the week due to Father's Day but later dropped. They fluctuated between 83,000 and 85,000 IRT per kg for Ecuadorian bananas and 66,000 to 69,000 IRT per kg for Indian bananas. The exchange rate was between 80,500 and 81,000 IRT to the USD.

The market expects that the ceasefire between Israel and Hamas and the hope of improvements in U.S.-Iran relations could positively impact the IRT.

Indian banana exports have faced challenges due to import license issues in Iran and chilling injuries to the fruit. The cost, insurance, and freight (CIF) prices for good-quality bananas not affected by chilling damage were around USD 8.00 per box, weighing 13.50 kg, CIF Bandar Abbas.

During the week, prices in the Ecuadorean Spot Market for the fruit alone ranged from USD 9.50 to USD 10.50 per box. These prices were influenced by the availability of ships of the regular shipping services to Europe and Russia. One vessel running on the Ecuador-St. Petersburg route arrived in Ecuador on Wednesday and was ready to load on Thursday, while another vessel for the same route was expected to arrive on Saturday.

Prices remained high due to lower volumes caused by a significant drop in production, estimated to be between 20% and 30% in some regions. This decline has been attributed to colder temperatures resulting from the La Niña phenomenon affecting the Andean country.

In the chartering market, several ships have been taken on Time Charter from operators or owners to meet demands, particularly in the citrus and grape trades.

Exports from South Africa are facing a shortage of available ships, as there is insufficient tonnage to meet the needs. Furthermore, there is a significant lack of specialized reefer vessels to accommodate the potential cargo requirements. The market could strengthen even further if the Falkland or southern Atlantic squid fishing demands more vessels.

One multinational company has extended a month-long contract for banana shipments from Central America to the USA. Another vessel has been secured to transport fish from Alaska to Japan, while another is set to carry fish from Poland to West Africa. Shipments of deciduous fruit from Argentina are expected to begin on January 31, leaving from San Antonio.

Current Time Charter rates for larger vessels range from US cents 100 to 105 per cubic foot (cbft) per month and US cents 100 to 110 per cbft per month. Ship owners request US cents 130 to 135 per cbft for contracts in January and February. Although these rates may not have been fully set up yet, brokers believe that if the squid fishing campaign in the Falkland and southern Atlantic regions is robust, rates could easily exceed US cents 135 to 145 per cbft per month due to the severe shortage of available ships. The recent ceasefire agreement between Israel and Hamas is a significant development, but its impact on international shipping through the Red Sea stays uncertain. Although the ceasefire is a positive development, the international shipping industry is likely to still be cautious until there is more certainty regarding the security situation in the Red Sea.

Despite the ceasefire, major ocean carriers are hesitant to return to the Red Sea due to ongoing security concerns. The region has been plagued by drone and missile attacks from Yemen-based Houthi militants.

Many shipping companies have rerouted their vessels around the Cape of Good Hope, which adds extra time and costs to their journeys. This trend is likely to continue until the security situation in the Red Sea improves significantly.

Bunker Prices:

VLSFO MGO

Rotterdam $554.00 $712.00

Gibraltar $594.50 $805.00

Panama Canal $600.00 $800.00